The world economy is in turmoil from the two unpredictable events of Covid-19 and war.

Russia, Belarus and Ukraine are all large players in the global timber trade and the war has greatly unsettled normal trade patterns. Russia had historically supplied a lot of sawn lumber into China and Europe; this trade has been dramatically altered by the war and is worsening. Europe and Australia are very short of lumber products which previously came out of Eastern Europe. Australia is no longer exporting logs to China, and South American supply has greatly diminished as it is unprofitable at current cost levels.

The beetle-damaged spruce trade from Europe is rapidly diminishing as salvage operations scale down. The European lumber market is also very much disrupted by the ban on Russian lumber, now classified as “conflict lumber”, meaning many end users are unable to use it in products which would previously have been certified as sustainable by third party auditors.

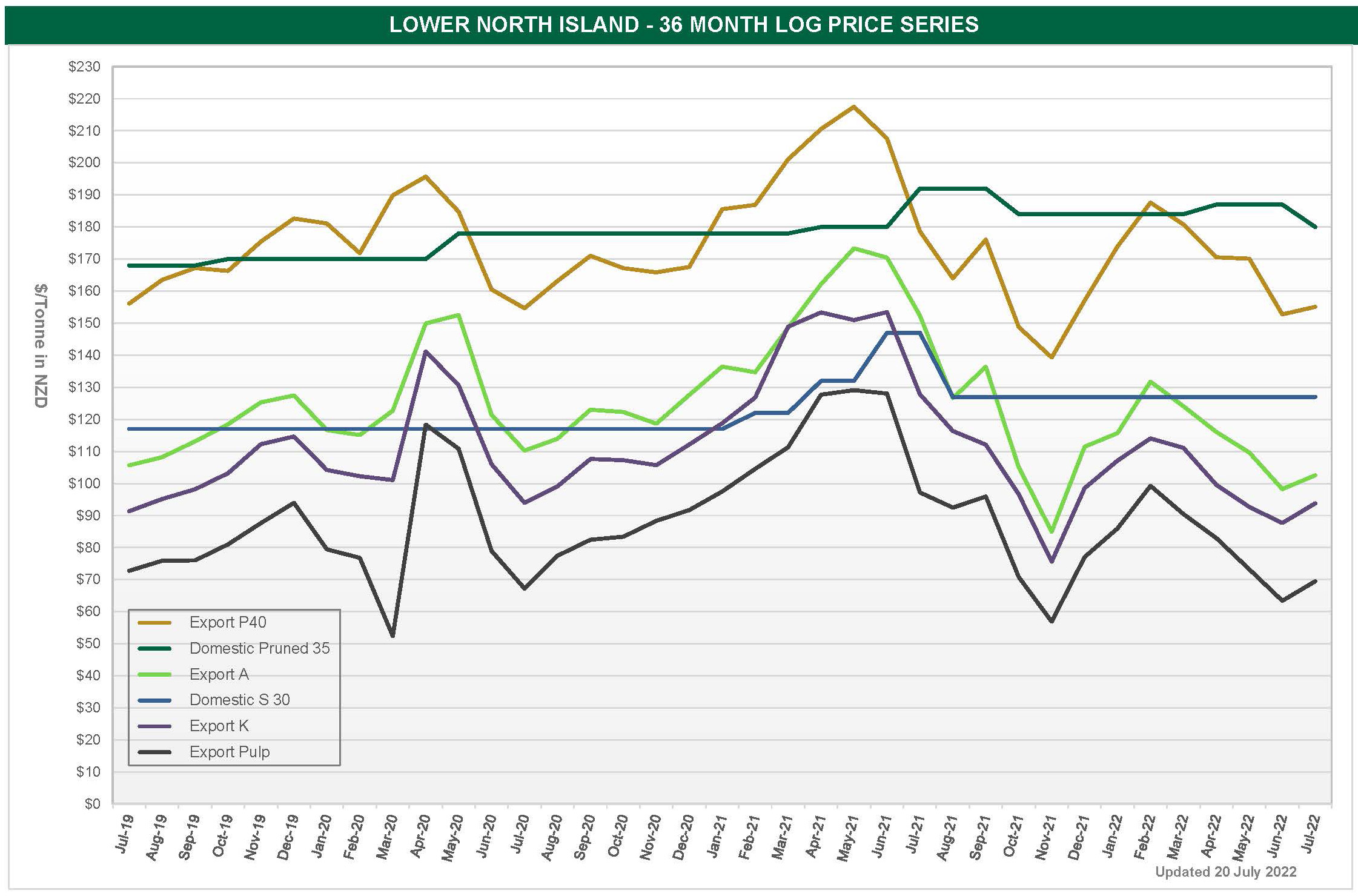

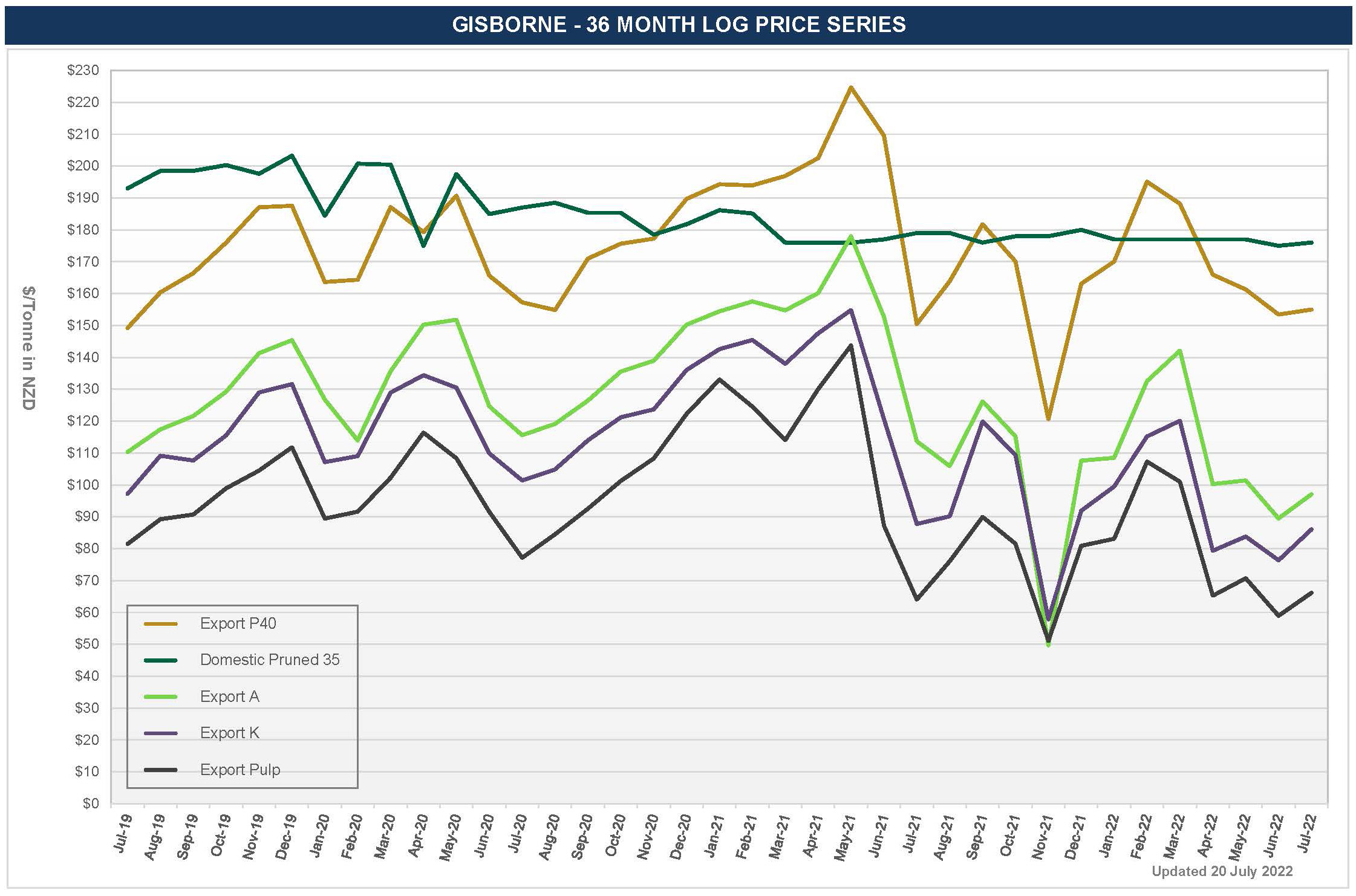

Export log markets are volatile with India and Japan at very low levels, and Korea slow. China is a very large customer for logs as their local forest resources are quite limited.

Demand in China is slow as Covid lockdowns cut industrial output. Log demand in China depends on the Covid-free status of discharge ports in China, as well as construction activity continuing in China. This lower supply and lower demand is coupled with increasingly high delivery costs from ship chartering and bunker fuel cost rises.

The diminishing log supply into China has meant prices are relatively stable despite reduced demand. Domestic sawmills continue to pay decent prices and show strong demand going into winter as local construction levels are high.

Seasonal and periodic disruptions to the log market are to be expected, and our response must always be prudent. We therefore reduced harvest production to 80% in our managed investment estate effective Monday 13 June, and we continue to monitor the market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}